The UK’s Day-Ahead gas price fell 2.3% to 12.60p/therm as higher than normal gas pipeline flows from Norway for this point in summer resulted in an oversupplied gas system. Towards the end of the week higher temperatures saw demand fall below seasonal normal.

Day-Ahead power rose 5.9% to £29.93/MWh, amid falls in anticipated power generation from renewables. According to a Reuters review, power generation from renewables have taken up a record share of global electricity production since the start of Covid-19.

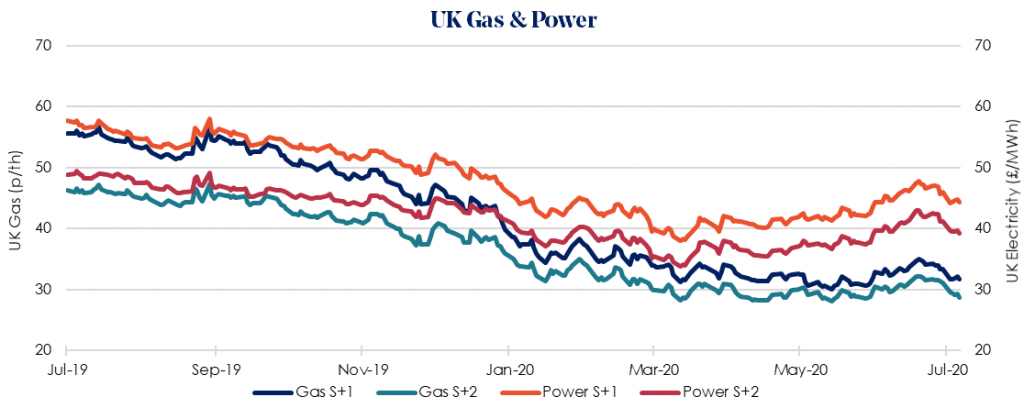

Winter 2020/21 gas fell 5.2% week-on-week to 31.62 p/therm, with the equivalent power price falling 3.6% to £44.28/MWh. Uncertainty over demand recovery continues to impact prices as the long-term outlook from Covid-19 remains unclear. This comes as several European countries including France, Spain and Germany saw increases in cases, prompting fears of a ‘second wave’.

Week-on-week losses were seen across much of the forward energy market, as the U.S. reached over 4.3 million confirmed Covid-19 cases, with over 1000 deaths for four consecutive days. Concerns remain that global fuel demand growth could stall.

Gas storage remains strong at around 84% full, compared to 64% typically seen at this time of year. LNG prices remained steady last week.

Maintenance is expected on Wednesday at fields delivering to the SEGAL pipeline from the North Sea, reducing capacity by 15mcm/d for two days.

Our recommendation remains to lock in contracts as soon as possible as prices are at risk of further increases following the easing of lockdown restrictions.