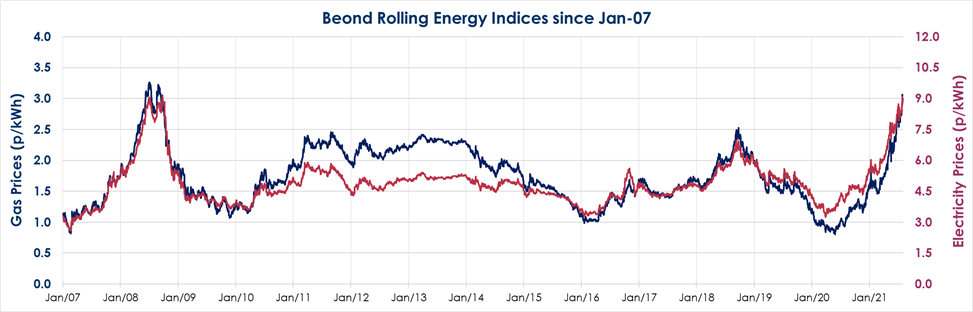

UK wholesale electricity and gas prices have reached prices not seen since 2008 when oil prices famously reached >$145/barrel. Customers who haven’t secured their contract already and need to sign a new contract before 1 October 2021 are asked: “why are prices so high?”, “what is going to happen next?” and “what are my options?”

With prices so high it’s easy to think that it’s only a matter of time before they drop. However, the reality is that prices are more likely to rise further over the next couple of months.

So in the short to medium term, high prices are here to stay. So if your renewal is coming up soon, it’s probably a good idea to get it locked away before prices go even higher.

However, once we get half-way through the winter period if there hasn’t been any major supply disruption we could see prices start to fall. But we don’t expect this to happen in any significant way until it’s too late for customers with 2021 renewals.

At some point in early 2022 we fully expect prices to drop significantly from the current highs. So clients with late 2022 renewals may be able to benefit from slightly lower prices next summer.

With prices having risen so high, it’s difficult for clients to know what they should be doing with their energy contract renewals. But Beond’s market outlook can help:

1 Oct 2021 and 1 January 2022 Renewals

| Option | Advantages | Disadvantages |

| Do nothing – go onto “out of contract rates” | You can sign a contract when/if the market falls | You’ll being paying 25+p/kWh for electricity and 5+p/kWh for gas. This option is not recommended |

| “short” 6 month fixed price contract | You can sign a contract in February or March. If we have a mild winter the market should have fallen by then | The cost will »15% more than a 12 month contract |

| 12 month fixed price contract | You can sign another contract in summer 2022, the market should be more favourable unless this coming winter (21/22) is very challenging | You have to absorb a significant price increase |

| “long” 24 month or 36 month fixed price contract | The cost will » 5% to 10% less than a 12 month electricity contract and for gas the saving is 10% to 20% | You are buying “year 2” and “year 3” at lower prices than “year 1” but the absolute prices are still relatively high |

| Flexible contract (for larger customers) | You can stagger your purchases and wait until later before buying 2022 | In the first six months the cost will be »15% more than a 12 month contract |

1 Apr 2022 Renewal

1 Oct 2022 Renewal (or later)

The above recommendations are indicative. Exact timing will depend on how the market evolves over coming months. Please speak to your account manager for an up-to-date recommendation.

If you would like to discuss the above further please do get in touch with Beond on 020 8634 7533 and ask for the strategic clients team.

The above information is supplied without any assumption of liability and you accept, by accepting the information, that we are not liable to you for your use of the information. While reasonable endeavours are taken to ensure that the information in this report is obtained from reliable sources, it is not guaranteed for accuracy. The views set forth are solely of those of the authors and not intended to provide advice or recommendations as the customer is solely responsible for its market decisions. Views expressed are subject to change without notice. The information must not be copied, distributed or published without our express permission.